Carbon Stuff - ESG v1 & v2 vs. the emerging Long/Short strategies

A letter I wrote to Matt Levine: Why the world of “more active bets” on the energy transition is happening fast

There’s no way that traditional ESG investing is going to make dirty CO2 emitting companies change their business practices, let alone their business model, but there are emerging models that might help do the trick… if activists and investors can agree how they work.

The whole reason I wrote that sentence requires some explanation first… Matt Levine is a very funny, very intelligent reporter at Bloomberg who writes about finance in his newsletter Money Stuff1. I read his pieces the moment they hit my inbox, and if I were a writer (instead of a non-writer who cares deeply about whether the world gets climate change right) I would aspire to be Matt Levine. I quote and misquote him frequently, though the only people to whom I quote him to have usually already read that day’s piece. You should understand this because I opened his column last Thursday to see a piece titled Someone is Going to Drill The Oil. “Oh, goody,” I thought to myself, “Matt Levine writing about the climate!”

So on Thursday I was nodding along through the first few sentences of his piece, and then I started shaking my head at the relative ink given to a line I don't agree with (‘ESG investments can drive up WACC for dirty companies’, which he’s not supporting but talking through a whole bunch) and only a couple sentences at the end I do buy (only regulation can save the day, and investors are underwriting that they eventually will), so I wrote this down to clarify my own thoughts, sent it to him in an email, and then realized that I needed to write this piece out. He responded immediately with a quick “all sounds reasonable and looking forward to learning more” and so I thought, well, if Matt Levine can learn something about this, I bet you all could too.

So here’s what I wrote Matt:

Dear Matt-

I find the proposition that traditional ESG investing would drive oil company behavior has been unlikely at best, and a convenient distortion at worst. It sounds like you may agree, but I wanted to tell you how I think behavior is going to be driven...

Chapter 1: ESG says “do good by not owning the worst stuff, and I’ll get the same fees!”

Though ESG asset managers have asked companies to provide an alphabet soup of data points and rubrics, their real effect has essentially been simply owning or not owning individual shares; it's binary. To say that a CFO cares deeply about whether ESG investors own his or her stock is to engage in deep self-delusion, unless it got to the point that ESG funds were such a huge proportion of the cap table that WACC increased. Not likely. Conversely, most ESG investors are not actually impact investors, but rather well-intentioned individuals and institutions who want to be told that their money is doing good. Since these asset owners are not in general particularly sophisticated on these issues, they're generally happy if they're told by asset managers that their funds are "doing good" because they're not invested in the worse. In other words, they credulously buy the idea that by being invested in ESG funds they are driving up the WACC of the "bad" companies (such as coal). ESG funds are kind of like divestment - the likely truth is that divestment of a company’s shares is largely ineffective unless it actually gets publicity and people stop buying a company’s products as a result2. You write again today about a way in which we delude ourselves about ESG’s effectiveness - Larry Fink, CEO of BlackRock, talks widely & compellingly about how we need to address climate change, but his funds are passive and mostly track big indices like the S&P500 etc, which include coal - so retail investors might even think they’re getting an ESG fund because they invest through BlackRock funds, but they’re still in coal. I’m absolutely not saying that BlackRock is trying to distort what investors think their money is doing. But I do think that the ESG investment industry overall has historically been saying “hey, give me your money, it’ll help the world get better”, when in fact they really mean is some form of “hey, give me your money over in this ESG pile instead of this other normal benchmark pile, and you can say you’re doing good because you don’t own the worst stuff, but I don’t have any real theory of action about why the world would get better if you didn’t own the worst stuff, and you get basically the same returns & I get the same (or even higher) fees, so we’ll all be happy, right?” In other words, any discussion of ESG funds driving up WACC seems to me to be a convenient mass delusion. It does make CFOs scurry around collecting data, but it hasn’t necessarily changed the behavior of many companies - in large part because so many factors are embedded in ESG rubrics. Excluding the worst emitters from your individual portfolio doesn’t drive their behavior - Exxon doesn’t care one tiny little bit whether you as an individual own it’s stock.

Chapter 2: “Instead of selling the worst stuff, I’ll own it and vote to tell managers to change what they do!”

Recently, however, we've seen a second chapter of ESG investing, where instead of divesting from the worst and chasing benchmarks, instead funds like Engine No.1 are investing and driving proxy votes at companies like Exxon to get climate-focused board members or binding resolutions to focus on climate costs. This is in the very early innings. However, what’s surprised a lot of observers is that passive investors like BlackRock (who as I mentioned above own these companies’ shares because investors tell them to invest in indices, and the indices own all the companies) got behind several of these votes and voted for change in board composition and strategy changes, despite historically backing management on most issues. And notably, these companies are beginning t clean up their portfolios, some by building more renewable energy to dilute their dirty portfolio, but also by selling off the worst stuff. However, as Larry Fink himself has pointed out, these assets which move from highly scrutinized public companies to private hands, emissions stay the same no matter who owns them. In fact, emissions may worsen as the dirty assets get sweated harder by more returns-focused owners who are "getting while the getting is good". Similarly, it appears that some petro-states like Russia and Oman may well be aiming to pump the oil faster faster before the Paris accords come for them.

But that begs the question, why are these companies & petro-states trying to move so fast to get oil out of the ground or to "clean up" their portfolios by selling off the worst assets? They too are underwriting the belief that carbon emissions may become scarce (in an economist nerd sense, meaning that they are expensive, outlawed, capped & traded, or any other version of scarce - you can’t have “emit all you want for free”, which is what we have today). If emissions become scarce, and emissions are an inextricable consequence of burning fossil fuels, then less fossil fuel will be burnt, supply will exceed demand, and the price of oil will plummet. That's what actually causes stranded assets - not well-meaning investors. And so, I agree with where you close Matt, that smart investors probably shouldn't buy oil assets even at low prices, because it’s going to be a bad bet (assuming we eventually make emissions scarce). When you see a private company like Hilcorp buying BP's North Slope assets, they are in effect underwriting that government won't get their act together and that the value of oil will remain high enough to justify pumping as fast as they can. That they may just be able to “get while the getting is good” or “pump while the pumping is good”. Inaction up until now would support that belief - but I sure think they’re running a pretty hefty risk. All these board changes and shareholder resolutions are evidence that I’m not alone - that a lot of shareholders are increasingly thinking that the bet on slow/never for effective regulation of emissions is looking like a really bad bet.

Chapter 3: Short the dirty companies, punish ‘em, and profit when carbon becomes scarce

However, at the same time there are a number of interesting hedge funds and who are making the opposite bet - that the energy transition will happen fast enough that you can reap significant rewards from betting on the cleaner / less carbon-intensive (measured in tons of CO2/$ of revenue) and against the dirtier / more carbon-intensive. There are a number of funds beginning to play this bet - including FFI's ETLS, and HITE Hedge's Carbon Offset fund. Both of these (and others that are emerging) are betting that those who produce dirty energy will lose and those who make clean energy will win. The strategy is pretty simple - create a portfolio that shorts (bets that the price will go down) all the highest carbon intensity companies within a sector like energy extraction, and buys (bets the price will go up) of all the companies that have lower carbon intensity. I’m not qualified to explain all the ins and outs - some products will be formulaic, some will be opportunistic, some will use more or less leverage. But the overall idea is that by shorting the “bad guys” (from a carbon intensity standpoint) you can create a fund that (a) has positive exposure to the scarcity of carbon and which profits from the energy transition, and (b) theoretically exerts downward pressure on a company’s stock price and increases its WACC. Please note the word theoretically in the prior sentence - you’d need a huge short position in these companies to really move them (which does happen from time to time, but exceedingly rarely in such large cap stocks), and this type of investment is unlikely to get enough capital behind it to move the needle either3. It’s better than the ESG v1, in that it theoretically does work to drive down a companies share price in a better way than just “not owning it”. And if you really wanted to have “zero exposure to carbon emissions in your portfolio”, you could achieve that by holding a set of ‘normal assets’, measuring the CI (carbon intensity per dollar of revenue) of those investments, and then hold an amount of this “long carbon” product that had positive exposure to the price of carbon equal to the negative exposure. But now we’re trying to do something moral (force the bad guys to change their behavior) with a tool of finance (reduce our exposure). And if you’re really getting to zero exposure by owning Chevron long in one hand and shorting it in the other… isn’t that effectively the same thing as not owning it all (ESG v1)? Of course, if you take your capital and invest more of it in these bets that carbon will become more scarce, then you are exerting some pressure on CFOs and CEOs of oil companies - but that is a concentrated risk that most institutional investors probably can’t make for fiduciary or incentive reasons!

Still, there's enough activity in this space that I'll be shocked if there isn't a fund-of-energy-transition-funds soon. These long/short bets have been very good strategies over the past few years, though they have been punished in 2021 as oil prices rallied4. It is likely a good strategy over the long term for very patient capital who believes in the theme that we will eventually get our emissions down close to zero, and for the impact investor who wants to drive us there faster. That brings us full circle to impact investors. Those who care about carbon now have an additional arrow in their quiver - they can "short the bad guys" instead of divesting (ESG Gen 1), or investing and voting (ESG Gen 2). In theory you give up nothing vs. benchmarks in either Gen 1 or Gen 2, and it's hard to imagine how you can drive behavior for free. Harvard's investment manager has come out with a proposal that he can get his portfolio to net zero by holding a standard portfolio, and then holding some shorts against the dirty guys. It remains to be seen if activists can be convinced that holding a short position on carbon to offset your long is the same as not holding any fossil fuel companies - what seems simple to someone versed in corporate finance isn't always obvious to someone who wants to change the world. It's also not clear just how accurately we can measure the carbon intensity of a portfolio, though carbon accounting companies like Persefoni sure are trying. But the fact that decarbonization approach Gen 3 is coming so quickly on the heels of Gen 2 is encouraging to me, because I think the mechanism has far more potential to drive management behavior, even if investors have to take some real bets vs. just “betting the market”. The interesting pattern here will be if we get enough significant investment on the bet that the energy transition will happen, they will have an incentive to push for it to happen faster… and that lobbying could be a very strong force indeed. So Gen 3 actually has a theory of action for why it might work to drive behavior. It remains to be seen if that theory of action can actually be a strong force, but unlike Gen 1, at least it could work and the incentives (and bet) are clear.

The real answer: only government can make carbon scarce

So to bring it back to where we started… There’s no way that traditional ESG investing is going to make dirty CO2 emitting companies change their business practices, let alone their business model, but there are emerging models that might help do the trick… if activists and investors can agree how they work.

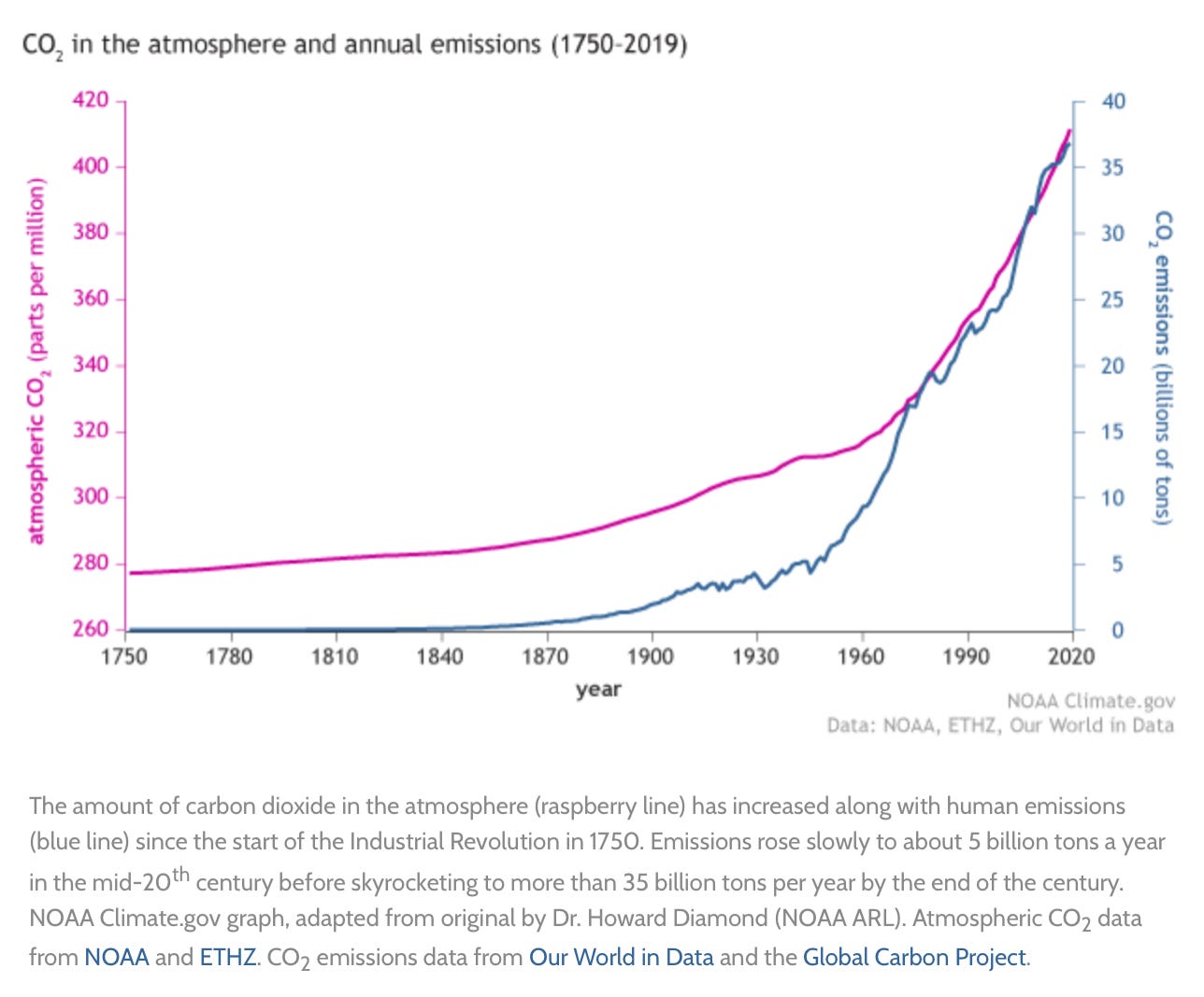

However, like you hint, Matt, the real reason that we might see truly stranded assets (oil and gas fields that are not profitable to ever pump again) is if the cost of regulation (price, cap & trade, tax, threat of jail time, etc) goes up high enough. No investors can make an investment a good investment or a bad investment just by investing in it or shorting it - the fundamentals win in the end. Still, markets are underwriting some future expectations of a non-zero carbon price and assets are trading hands based on those expectations. When they turn out to be right (and they'd better, else we'll likely never succeed in getting the "blue line" in the below annual emissions graph down to zero in the next couple decades), the asset price dislocations are going to be crazy. And then, Gen 1 and Gen 2 are not going to look very good vs. Gen 3 (short the bad guys, long the less bad guys). But being eventually right sucks if you die first, so governments really have to get on the ball.

^^ the "blue line" above is annual global emissions, and the pink line is the amount in the atmosphere. Net zero means that the blue line comes down to zero within a small # of decades, after rising and accelerating for 200 years. I know you know that, but the picture focuses the mind. “Addressing global warming means nothing more nor less than getting the blue line down to zero in the next 2-3 decades”.

-John

So, a big thanks to Matt Levine for writing the piece that got me off my behind to lay out something I’ve been thinking about for a while, and I hope he - and you - got something from it. I’d be interested in comments and thoughts - this space is emerging very rapidly (heck, v2 didn’t exist a few months ago, and v3 is pretty raw too).

If you get nothing else out of this, I do hope that you sign up for his newsletter. He has been doing this for LONG before there was such a thing as substack, and I always learn something. And even when I don’t learn something, I read it anyways because he’s hilarious. I realize that I sound like a fanboy. I don’t aspire to having 150k subscribers, or whatever he has now, but if I can make decarbonization engaging and simplify it for people who want it to happen, think it needs to happen, or want to make sure that they can still have a living when it does happen, I’ll be pretty pleased.

The article to read on divestment is William McCaskill’s Does Divestment Work from the New Yorker in 2015. Not that it’s uncontroversial, there are certainly people who think that it does work (or that it works indirectly as a PR lever), but it’s crystal clear in it’s reasoning.

At least not until its a foregone conclusion that carbon scarcity is going to drive the price of oil down inexorably to zero, at which point we’ve already achieved what we set out to do.

One super simple way to put it is that these are really concentrated bets against carbon emissions continuing to be free. I’m not a well-educated enough finance person to really understand why if you get enough short bets against a currency it eventually has to devalue. Here you’re making bets that the price of relatively carbon-intensive companies will go down. The set of linkages to imply that hence the price of carbon will go up seems harder for me to believe. If this is your speciality, please write me or comment because I’d love to understand whether & how this could work.

I looked into how retail investors can get into this strategy and wonder if you could compare notes. From what I can see, FFI's ETLS is available on the SmartX platform and requires an RIA to get involved with a $60k minimum. (It's also possible to get involved as a qualified investor, but that requires a net worth of >= $5 million. HITE Hedge's Carbon Offset fund has a $250k min.

How would you describe https://carboncollective.co's strategy? To me, it resembles the long-half, but not the short one.

Hey - I just really appreciate you putting out these this type interesting analysis. It doesn't seem like it's reaching a wide audience all of the time, but I'm personally very glad that it's at least reaching me. Please keep up the good work!